Key Takeaways

- A Limited Liability Company (LLC) offers the best liability protection. Its flexible management makes it an appealing option for many other business owners and entrepreneurs worldwide.

- LLCs protect members’ personal assets from the majority of business debts and legal claims, helping to lower the financial risk of business owners.

- LLCs provide you with very versatile taxation options. There’s the fact that members can elect pass-through or corporate tax treatment which is advantageous to both resident and non-resident members.

- Compared with corporations, LLCs have a lower burden of formalities and ongoing paperwork, thus a lower day-to-day operational complexity.

- Whatever state you’re in, forming an LLC is pretty easy, particularly with honest, hardworking services such as Northwest Registered Agent. Selecting a state with less intimidating fees will help save you money during the process as well!

- Understanding the benefits and potential drawbacks of LLCs helps business owners select the right structure for their needs and ensures compliance with local and international regulations.

Listen to This Topic on the Startupsole Podcast

An LLC, or limited liability corporation, protects owners against personal liability. It makes maintaining business logic straightforward.

It combines attributes of corporations and partnerships, allowing individuals to pool their efforts and benefits. LLCs are effective for small and large collectives, and regulations may vary by nation or state.

It’s no wonder that entrepreneurs choose LLCs for their tax simplicity and straightforward regulations. The following section explains what an LLC is and some of the most important aspects of an LLC.

What is a US Limited Liability Company?

It melds the liability-limiting aspects of corporations with the nimbleness of operations typically found in partnerships. This balance makes LLCs an attractive option for business owners who want to protect personal assets without a complex day-to-day management structure.

LLCs can have an unlimited number of members. Best of all, there’s no need for any members to be US citizens! This transparency serves to empower business owners. Combined with a flexible management structure, it provides them with much greater latitude in how they operate and develop their business.

1. LLC Meaning: Breaking It Down

LLC stands for “Limited Liability Company.” Specifically, it is a business structure that is legally separate from its owners. An LLC offers liability protection, which a sole proprietorship lacks.

This provides a strong layer of protection, as owners’ personal assets are generally protected if the business incurs debts or is sued. Owners are not putting their home or car on the line if the business goes under. To create an LLC you need to file your articles of organization with your chosen state.

Apart from that, you must cover a filing fee and designate a registered agent.

2. The Big Deal: Personal Asset Shield

LLCs guard their members from personal liability for company debts or claims. So, for instance, if an LLC is sued, only the assets of the business would be in jeopardy.

There are limited situations where courts will “pierce the veil,” but these are the rare exceptions. This shield allows entrepreneurs to do their thing with far fewer worries about personal financial ruin.

3. Tax Flow: How Money Moves

First, by default, the IRS does not tax LLCs directly. By default, single-member LLCs are “disregarded entities,” and multi-member LLCs are taxed as partnerships.

This makes the process easier because members simply report income on their individual tax returns. Of course, LLCs can elect to be taxed as corporations. Non-US residents may be members of an LLC, but keep in mind that they will still need to comply with US tax laws.

4. Unique Structure: Not Quite Corp/Partner

LLCs can avoid a lot of those formalities, such as holding annual meetings. Business owners, known as members, are free to operate the company themselves or appoint managers.

This arrangement is suitable for individual endeavors or significant assemblies.

5. Who Needs an LLC, Really?

LLCs are well-suited for independent freelancers, small mom-and-pop operations, family businesses, and large collectives. They provide liability protection and are easy to maintain.

Overall, risk-averse owners tend to prefer LLCs because they provide an asset shield.

6. Global Context: Similar Ideas Worldwide

Other countries have parallel structures, like the UK’s LLP or Germany’s GmbH. Every area has its own laws and regulations, but the essential principle—reduce owner liability, provide flexibility—remains constant.

Top Reasons People Choose LLCs

With their combination of liability protection, flexibility, and simplicity, it’s no wonder that most business owners today choose LLCs. LLCs can help insulate you from certain business-related risk, while still allowing you to maintain control over how your business is operated. The infrastructure is conducive for mom-and-pop shops, corporate departments, high-tech incubators, and multinational merchants.

When you create an LLC, you establish your business as serious and legitimate in the eyes of the public—not just a gig.

Your Personal Stuff Stays Safe

LLCs protect your personal assets, such as your home or savings, if your business gets sued. If you get sued over something your business did or had, only the business’ assets are at stake. Owners typically aren’t personally liable for business debts.

So, for instance, if a customer were to slip and fall in your store and file suit, your personal savings are safe from being touched. That’s reassuring, allowing you to concentrate on what really matters—growing your business.

Flexible Tax Choices Available

LLCs enjoy a big tax perk that pass-through entities have. You have the flexibility of passing revenues and losses directly to your personal tax returns, or electing company-level taxation. That’s because you escape double taxation.

For non-US owners, they tend to choose LLCs so that they pay taxes only on their US income, not their worldwide income. This facilitates effective global tax planning and can result in significant cost savings.

Easier to Run Day-to-Day

LLCs are easy to operate. You don’t have to hold annual board meetings and deal with tons of red tape. Owners are free to make everyday decisions without extensive bureaucracy.

Even in states with a report, the burden is minimal compared to nearly all other businesses.

Looks More Professional

Another reason is that having “LLC” after your name gives your business an air of professionalism. Banks, clients, and partners prefer to do business with legally established entities.

This makes all the difference in landing large contracts or new customers.

Great for Solo or Teams

LLCs are great whether you have one owner or several. You can distribute profits however you prefer, and it’s easy to add new partners with minimal hassle.

This accommodates a lot of business models, from one-person operations to companies operated by a family or team.

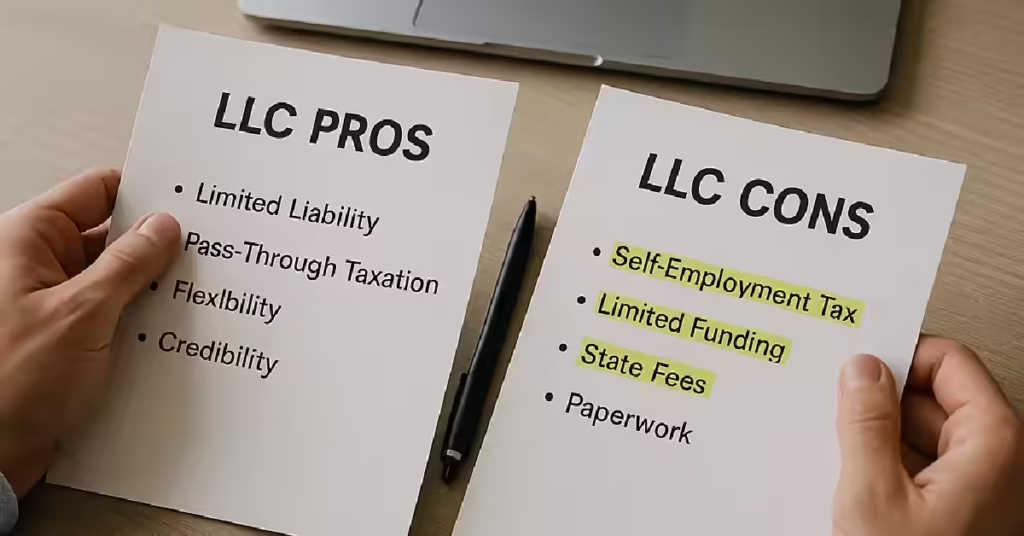

Are There LLC Downsides?

LLCs provide a tremendous advantage for most, but there are three main trade-offs. It’s important to acknowledge LLC downsides too. Before you create an LLC, it’s good to consider pros and cons. These downsides are not universally true for all businesses and/or the purposes they seek to achieve. Understanding them ahead of time will make for better preparation on your part!

Potential for Higher Taxes

In fact, some LLCs pay more in taxes than corporations do, depending on where they are located and how they are structured. Members are subject to self-employment taxes on their share of profits, which can quickly amount to a hefty sum.

For instance, a small design professional firm based in the U.S. Might end up paying more in self-employment tax. This is usually the case as opposed to an equivalent business organized as a corporation. Getting in front of these things—such as by collaborating with a knowledgeable tax professional can reduce this tax burden, though no single solution will work for everyone.

Can Get Complicated Fast

An LLC with multiple members can quickly become complicated. Having a well-drafted operating agreement that governs the LLC is important, but it’s not that simple.

Without explicit guidelines, responsibilities and roles quickly become muddled. State rules can create additional hurdles, such as requiring annual reports or fees. Under certain circumstances, if a member withdraws or passes away, the LLC can dissolve unless preventative measures are adopted from the outset.

Funding Can Be Tricky

LLCs can have a difficult time raising capital. Investors sometimes like them corporations, which can provide shares.

Transferring ownership isn’t always easy, which can spook outside capital. Venture capital is uncommon for LLCs, but other forms such as loans or grants may be more appropriate.

Not Always Best Fit

LLCs are not appropriate for all businesses. For fast-growth tech firms or those targeting large sunk-cost investment, a corporation may be the better fit.

Not every business is best suited to an LLC.

Forming Your Own LLC: The Steps

It’s easier than you think. Setting up an LLC just involves a few straightforward steps. Each step serves to ensure that your business is off to a great start while adhering to your state’s regulations. Most steps are pretty straightforward, particularly with the help of LLC formation services, such as Northwest Registered Agent.

States like Wyoming and New Mexico are favorites among non-residents for their low costs and streamlined processes.

Pick a Unique Business Name

Your LLC will require a name that’s both eye-catching and adheres to state guidelines. Look up the availability of your desired name through your state’s online database. The name can’t be the same as any other business and must contain “LLC” or an equivalent designation.

Pick a name that’s catchy, easy to pronounce, and gives an idea of what your business will be.

Designate Your Registered Agent

A registered agent is required in each state you plan to do business. This individual or entity receives legal documents on behalf of your LLC. The agent needs to have a physical address in the state.

To be clear, timely response is always critical. The majority choose Northwest Registered Agent because we provide consistent, trustworthy service.

File Official Formation Papers

This usually requires you to file articles of organization with the state. This form provides important, basic information about your LLC.

Double check all information before submitting! This is an official formation document, so keep a copy for your records. It’s a time-saver that reduces stress.

Draft Your LLC Operating Agreement

An LLC operating agreement is an internal document that establishes guidelines for your business’s operations. It addresses ownership of the business, member responsibilities, and how decisions will be made.

Even single-member LLCs benefit from having one, for the sake of clarity and to avoid future disputes.

Get Required Business Licenses

Some industries require additional licenses or permits. These vary based on your industry and location. Local licenses are usually unnecessary for online businesses operated by non-residents.

So, make sure you confirm and do your research.

Understand Initial Filing Fees

LLC formation costs can vary greatly. Others, such as Wyoming and New Mexico, only charge around $50–$100.

Understand your ongoing cost requirements. Plan on yearly fees as well, like annual reports or franchise taxes in some states.

Single Owner vs. Team LLCs

The crux of any limited liability company is the ownership structure. There are single-member LLCs, owned by a single individual, and multi-member LLCs, with two or more owners, called members. Each structure determines how decisions are made, how profits are distributed and how the work is divided. Understanding these distinctions allows business owners to choose the option that best meets their needs.

Going Solo: Single-Member LLCs

Going Solo: Single-Member LLCs A single-member LLC assigns control to just one individual. This arrangement is straightforward and transparent. The owner gets to decide everything and doesn’t have to consult anyone else.

It makes actually running the business – and filing taxes – much simpler too. Usually, the sole proprietor is able to pass through business income and losses on their individual tax return. This reduces administrative burden.

In addition to pass-through taxation, there is personal liability protection, meaning the owner’s personal assets are protected from business debts. Single-member LLCs work well for freelancers, consultants, and non-US residents who want to start a business with flexible tax options.

Partnering Up: Multi-Member LLCs

Multi-member LLCs are formed by two or more owners joining together. Working as a team can provide more creative solutions and greater capital. Profits and losses can be divided however the members prefer.

Well-defined agreements are important to establish roles and responsibilities and to avoid confusion down the road. All members receive liability protection; however, one member’s actions can impact the liability of the remaining members.

We understand that good communication is essential and all partners need to be prepared for collaborative decision-making. If one member leaves, the LLC can usually continue to operate.

Who Makes Decisions Here?

Under single-member LLCs, the owner calls all the shots. In typical multi-member LLCs, members are required to vote on major decisions. Voting rights and rules should be established at the beginning.

This prevents infighting and keeps the company focused on growing the business. When smart people get to work, creating consensus should be priority number one.

How Agreements Shape Operations

Operating agreements dictate how each LLC operates. These agreements detail how issues are addressed, who is responsible for implementation, and how amendments are adopted.

Properly addressed, each LLC has an opportunity to craft its agreement that best suits its own operations. It’s wise to check in and amend these rules regularly, so they are always reflective of the business.

LLC Taxes: The Simple Version

LLCs provide a more attractive tax structure that many entrepreneurs appreciate. Unfortunately, this freedom comes with the responsibility for members to know how taxes will affect their business. There’s no one right answer for every LLC. This choice has a big impact on how money can flow between the business and its owners.

An accurate understanding of these options is essential for members to comply with tax regulations and maintain operational efficiency.

Default Tax Treatment Explained

A single-owner LLC defaults to being taxed as a sole proprietorship. In contrast, a multi-member LLC is treated for tax purposes as a partnership. This means that all profits pass directly through to the members, who then each report their share of that income on their individual tax returns.

For multi-member LLCs, it’s the same as for a partnership. The business must file Form 1065 and provide a Schedule K-1 to each member. This means that members pay self-employment tax, currently 15.3%, which is divided between Social Security and Medicare.

Being aware of your tax status can help you plan for your tax payments and avoid an unexpected tax bill.

Option: Taxed Like a Corporation

LLCs can elect to be taxed like S-corps or C-corps. With an S-corp, owners can reduce their self-employment tax by taking a combination of salary and dividends. In order to accomplish this, you have to file IRS Form 2553.

If taxed as a C-corp, the LLC is subject to a flat 21% federal income tax on net income. Profits that are paid out as dividends can be taxed a second time. A tax pro should be able to quickly illustrate which option works out best.

Yearly Tax Duties: What to Expect

Yearly Tax Responsibilities—What to Expect LLC members need to regularly report profits, pay taxes, and file forms. Timely filing, good recordkeeping, and staying abreast of changes in tax law are crucial.

Payroll taxes need Forms 940 and 941. In most states LLCs are required to pay annual fees or franchise taxes. For instance, California has a minimum $800 annual tax, plus additional fees according to income!

State Taxes: A Quick Look

As with many aspects of the law, each state gets to make its own tax rules. Some levies annual LLC taxes. Tax rates, deadlines, and potential write-offs differ, so review regional regulations.

Failing to understand these might mean you lose out on significant savings or face costly penalties.

Watch Out for Underpayment Issues

If you underreport your income or fail to make your payments, you will incur penalties. Proper record-keeping ensures they are well documented and protects you from liability.

Take care of business in advance. Finding errors before they happen is the best way to avoid penalties.

Keeping Your LLC Healthy & Active

Life doesn’t end once you form an LLC and open the doors to your business. As you can see, there’s a number of important ongoing steps required to keep your LLC healthy and active—all of which are crucial for long-term success and compliance.

You will need to adhere to state requirements and stay on top of filings. Plus, keep tabs on financials and changes in the law that may impact the business. Conduct daily stand-up meetings to go over what’s on your plate and work through challenges.

Utilize checklists and calendars to help stay organized and timely! Free and open communication between group members will allow team members to identify issues early in the process and collaborate more effectively.

Regular Reports and State Filings

LLCs should be aware of the regular reports and state filings required by whatever state they conduct business in. These are usually annual, though occasionally biennial reports and due dates can vary wildly from jurisdiction to jurisdiction.

Failing to meet these deadlines could result in your LLC incurring additional fees. In addition, it might even forfeit its good standing, which can impact its capacity to operate or expand.

Maintaining clear records, like meeting minutes and amendments to contracts, aids in the filing process. It keeps the LLC in good standing with the regulations.

Keep Business & Personal Separate

If you mix business and personal funds, you might create major issues for your LLC. In order to protect the LLC, you need to establish a separate business bank account.

By doing this, all of your spending and income will always be easy to see. This additional benefit protects owners from personal risk while ensuring the LLC’s liability shield remains intact.

Avoid “Piercing the Veil” Risks

When an LLC fails to abide by its own regulations or commingles funds, courts can “pierce the corporate veil.” This can lead to owners being personally liable for liabilities and debts of the business.

Following formal procedures, maintaining thorough documentation, and conducting business transparently can mitigate this risk.

Dealing with a Suspended LLC

Once an LLC is suspended, it’s no longer allowed to operate legally. Resolving this typically requires filing delinquent forms, paying associated fees, and in some cases, proving that all regulations are being followed today.

It’s always best to monitor your LLC’s status regularly and address any issues as they arise.

Properly Dissolving an LLC

Shutting down an LLC the right way means following the state’s steps, telling all partners, paying debts, and recording the process. Since each state has its own unique dissolution process, following the process your state requires to the letter is critical.

LLC vs. Other Business Structures

Deciding on a business structure largely determines how a business operates, is taxed, and limits liability. LLCs are unique in that they provide liability protection, tax advantages, and fewer bureaucratic hurdles. Here’s a look at how LLCs stack up to other popular business structures.

We’ll dive into why it’s important to make the right choice to meet various business needs.

LLC or Sole Proprietorship?

LLCs protect business owners from personal liability. If the business ever accrued debt or dealt with a lawsuit, owners’ personal assets such as their homes or savings remain protected. As you can see, sole proprietors are at great risk.

If their business gets in trouble, all their personal assets are at risk. Both passes through to their owners, so both are subject to pass-through taxation. Unlike other business structures, LLCs enjoy the flexibility to elect their tax treatment, giving them more control.

Running an LLC means more paperwork than a sole proprietorship but lets owners set up rules and roles, so things run smoother. When deciding between these, consider your risk tolerance level.

LLC or General Partnership?

General partnerships divide control and profits among partners, but—unlike an LLC—each partner is personally liable for business debt. LLCs prevent all their members from personal liability.

LLCs offer more flexibility in terms of management – partnerships tend to function on the basis of equal decision-making authority and profit-sharing agreement. In an LLC, many of those disputes that are common in partnerships can be avoided.

They do that by making it clear up front in an operating agreement.

LLC or S Corp/C Corp?

LLCs provide for pass-through taxation, bypassing the double taxation that C Corps experience. S Corps pass profits through but have more stringent regulations on ownership and structure.

Corporations require a board of directors, yearly meetings, and a plethora of documentation. LLCs are a much less formal structure, with fewer requirements, rules, and paperwork.

One advantage corporations have over LLCs is the ability to easily raise capital through the sale of stock. All of these structures have liability protection, though corporations can occasionally lose this protection if certain rules are not adhered to.

Common LLC Mistakes to Sidestep

In addition to being a great asset protection option, setting up an LLC provides ultimate flexibility. Unfortunately, many of these individuals get caught in pitfalls that can waste their time, money, and serenity. By understanding these common errors, business owners can ensure they remain on the right path and their LLC remains in good standing.

Skipping the Operating Agreement

Too often, they skip an operating agreement, unaware that the document establishes the basic guidelines that govern how the LLC operates. Without it, members could dispute their roles or how to divide the profits.

For instance, if two friends go into business together and overlook this step, they may hit a wall over major decisions down the road. It should be tailored to the LLC’s specific arrangement, indicating who’s in charge of what aspect and how the agreement will evolve should one member exit the agreement.

Mixing Money: A Bad Idea

Combining personal and business funds is bad news. This mix can shatter the shield that protects owners from business liabilities.

Having distinct types of bank accounts helps you have a clearer flow of money and clearer records. This sort of organization proves invaluable should your LLC ever be hit with a tax audit or lawsuit.

Ignoring Ongoing Compliance Rules

Each state has its own ongoing rules required of LLCs, such as submitting annual reports or paying state-level fees. Failure to file a report may result in monetary penalties or the forfeiture of the company’s legal existence.

Most states use these reports to keep their business registries up-to-date and accurate. Thus, make it a point to check the rules regularly.

Misunderstanding Liability Limits

Sure, your personal assets are generally protected if your LLC is sued, but not always. If, for example, an LLC member commingles funds or engages in illegal behavior, personal assets can be exposed.

Business owners who understand what the law encompasses can better protect themselves from liability exposure and budget for unforeseen circumstances.

Forgetting Annual Requirements

Failing to file annual requirements or meet certain deadlines may dissolve an LLC. Proper record-keeping ensures each deadline is met and prevents the business from coming to a grinding stop.

Conclusion

LLCs suit a wide range of projects and missions. They provide protection from risk and allow individuals to choose how to manage their tax burden. Residents appreciate the low maintenance requirements and certainty of regulations. LLCs are beneficial for solo owners as well as teams. Filing to form an LLC remains easy for the majority, but mistakes can still catch first-time owners off guard. Each configuration has its advantages and considerations to be aware of. Regulations and taxation vary by state and require careful consideration. Looking to launch or grow your smart city business? Scan the state regulations. Consult a professional if you require assistance, and follow the advice listed above to determine what to do next! Good decisions go a long way toward protecting your business.

Frequently Asked Questions

What is an LLC?

An LLC, or Limited Liability Company, is a relatively new business structure in the United States. It provides legal protection for the owners, or members, keeping personal assets safe from company liabilities.

Who can form an LLC?

This means that almost anyone can form an LLC, whether you’re an individual person or a group of people. You don’t have to be a U.S. Citizen, although some state-specific restrictions may apply.

Is an LLC good for a single owner?

If so, the answer is yes, a single owner can create what’s known as a “single-member LLC.” It offers personal liability protection and easy tax filing.

Are there disadvantages to LLCs?

LLCs are usually more expensive to form and upkeep than other business entities. Other states charge money and/or mandates yearly filings and/or reports.

How are LLCs taxed?

LLCs typically enjoy “pass-through” taxation. This allows profits and losses to “pass through” directly to owners, who are responsible for reporting them on their personal tax returns.

Can I convert my business to an LLC?

Can I convert my business to an LLC? Like any other business formation, the conversion process requires lots of detailed paperwork and a filing fee.

What mistakes should I avoid with an LLC?

Two mistakes we see all too frequently are forgetting to file your annual reports and mingling personal and business financials. These can jeopardize your liability protection.